Health insurance is an important aspect of life in Michigan. Understanding the different types of health insurance, key terms, availability, and cost is vital to finding the right policy for you. Shield Insurance Agency understands the importance of finding the best health insurance plan for you and they have the expertise to help determine the best coverage to fit your needs. Read on to learn more about health insurance in Michigan, including HMOs, PPOs, HRAs, HSAs, and more.

HMOs and PPOs

Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs) are two common types of health insurance. HMOs are health insurance plans that provide access to a network of healthcare providers and usually require referrals in order to see a specialist. PPOs also provide access to a network of healthcare providers, but they allow you to choose your own doctors and do not require referrals. Both have different structures that affect how much you pay for services and how much deductible and copayments you pay.

HRAs and HSAs

Health Reimbursement Arrangements (HRAs) are employer-provided plans that allow employees to set aside pre-tax dollars to use for eligible medical expenses. Health Savings Accounts (HSAs) are also employer-provided plans that allow employees to save pre-tax dollars to use for eligible medical expenses. They are similar to 401k accounts, in that investments are allowed and the money rolls over from year to year. Both of these accounts can be used to help pay for out-of-pocket medical expenses, such as copays and deductibles.

Key health insurance terms

When thinking about health insurance in Michigan, there are several key terms to keep in mind. Copayments (or copays) are fixed amounts that customers pay for services, such as doctor visits or prescriptions. Deductibles are the amount of money the customer pays out of pocket before the insurance company pays for services. Coinsurance is the percentage of costs the customer pays once the deductible is met.

How much does health insurance cost

The cost of health insurance is different for everyone depending on factors such as age, family size, location, and type of plan. Generally speaking, HMOs tend to be less expensive than PPOs, and the higher the deductible, the lower the monthly premium. Health insurance premiums also depend on whether or not you receive subsidies or tax credits. In Michigan, the average monthly premium for family coverage with an employer-sponsored plan is about $735.

What are the different health insurance metal levels are

Health insurance plans also differ from one another depending on their level of coverage. Platinum plans typically have the highest premiums but also the most coverage, while bronze plans have the lowest premiums with the least coverage. Silver and gold plans are in the middle, offering somewhere between the two extremes of platinum and bronze plans.

When you can buy health insurance

The Annual Open Enrollment Period (OEP) is the time when everyone can buy a health insurance plan or make changes to their existing plan. In Michigan, the OEP runs from November 1st through December 15th each year. If you miss the OEP, you can still buy coverage outside of open enrollment if you experience certain life events, such as marriage, the birth of a child, or a move to a different state.

Where you can buy health insurance

You can buy health insurance from Shield Insurance Agency which represents over 40 insurance companies and specializes in helping individuals and businesses find the right plan for them. They can help determine the best level of coverage and answer any questions you have about health insurance in Michigan. Contact Shield Insurance Agency at (616) 896-4600 for a free quote today or start the quoting process by visiting this LINK and an agent will be in touch soon.

Health insurance in Michigan is an important aspect of life and it is essential to understand the types of health insurance, key terms, availability, and costs when shopping for a plan. Shield Insurance Agency has the expertise to help guide you through the process of finding the right policy for your needs and they can provide a free quote. For more information about health insurance in Michigan, contact Shield Insurance Agency at (616) 896-4600 today or visit this LINK to start the quoting process.

The Roommates You Never Knew About (A Deep Dive Into The Insects That Live In Your House)

Unless you’re an entomologist, the thought of sharing your home with insects might not be a pleasant one. But the truth is, there are probably more insects living in your house right now than you realize.

So, let’s take a closer look at some of the most common insects you’ll find in your home so you can take pest control steps to get rid of them once and for all.

Bedroom Hiding Spots for Insects

From the cracks in your floorboards to the gaps between your furniture, there are countless hiding spots for bugs to take refuge in your bedroom. Plus, bedrooms are often full of dust, which provides a food source for many types of insects. And finally, most bedrooms are located near other rooms in the house (such as the kitchen or bathroom), making it easy for pests to travel from one room to another.

Bathroom

The bathroom is one of the most commonly used rooms in any home, and it’s also one of the most likely places to find pests. From ants and cockroaches to spiders and silverfish, a variety of creatures are drawn to the humid, dark environments found in bathrooms. In many cases, these pests are simply looking for a source of water or shelter. However, they can also be attracted by the food left behind on counters and in sinks.

Common Areas

Your living room is a gathering place for your family and friends. It’s also a common gathering place for bugs. Why are there so many bugs in your living room? There are a few reasons.

First, your living room is usually one of the warmest rooms in your house. Bugs are attracted to warmth. Second, there are usually lots of food and water sources in your living room. Third, there are usually lots of hiding places in your living room.

Finally, your living room is usually full of people coming and going. Bugs can hitch a ride into your living room on clothing or shoes.

VIDEO: Humpback whale almost swallows kayakers near a California beach

The two managed to escape unscathed, briefly going underwater after capsizing before reemerging.

Julie McSorley says she learned an important lesson after she and her friend ended up in a humpback’s mouth: “Whales need their space.”

McSorley and Liz Cottriel were kayaking together in California’s San Luis Obispo Bay watching the whales feed on silverfish when one of the massive sea creatures surfaced beneath them, toppling their kayak and knocking them into the water.

Videos and photos from other kayakers and paddlers appear to show the women and their kayak being momentarily engulfed in the whale’s mouth — though the two friends say it all happened too fast for them to be sure.

“It’s definitely woke me up to the realization that, you know, our place is not in the feeding zone of whales,” McSorley told As It Happens host Carol Off.

“We didn’t think we were that close, but we definitely were right in the area that we shouldn’t have been — so I’ve learned my lesson, big time.”

Swallowed By Whale

AVILA BEACH, Calif. — Two whale watchers had a close encounter while kayaking off the coast of Avila Beach, California, that they will likely never forget.

Julie McSorley and Liz Cottriel were watching humpback whales on Monday when one decided to get up close and personal. A whale came up underneath them and caused them to capsize.

“I saw the big pool of fish, the big bait ball come up out of the water,” McSorley told CNN affiliate KMPH. “I saw the whale come up. I thought, ‘Oh, no! It’s too close.'”

“All of a sudden, I lifted up, and I was in the water.”

Footage from a witness nearby makes it appear as if the kayakers are being swallowed by the whale, but the two just tipped over.

“The whale was right here in my face, literally,” Cottriel told KMPH.

“I’m thinking to myself, ‘I’m gonna push. Like, I’m gonna push a whale out of the way! It was the weirdest thought. I’m thinking, ‘I’m dead. I’m dead.’ I thought it was gonna land on me. Next thing I know, I’m underwater.”

The two managed to escape unscathed, briefly going underwater after capsizing before reemerging.

Humpback whales typically feed on krill and small fish, according to the National Oceanic and Atmospheric Administration (NOAA).

The NOAA says humpback whales are popular among whale watchers as they are active on the surface and often jump out and slap the water with their pectoral fins or tails.

Medical expenses can be a significant financial burden, especially if you or a family member requires extensive medical treatment. Health insurance is a crucial tool that can help you manage these costs and ensure that you and your loved ones receive the care you need. In this blog post, we will explore the different types of health insurance available, the benefits of having health insurance, and how to find affordable coverage.

Types of Health Insurance

There are two main types of health insurance: private health insurance and public health insurance. Private health insurance is typically purchased by individuals or provided by employers as part of a benefits package. Public health insurance is provided by the government and includes programs like Medicare and Medicaid.

Supplemental health insurance is another type of coverage that can be added to your existing health insurance plan. This type of insurance can help cover costs that are not included in your primary health insurance plan, such as deductibles, copayments, and coinsurance. Benefits of Having Health Insurance

The primary benefit of having health insurance is protection. Health insurance can help cover the costs of medical treatment, including doctor visits, hospital stays, and prescription medications. Without health insurance, these expenses can quickly add up and become Unmanageable.

In addition to financial protection, health insurance can also provide peace of mind. Knowing that you and your family are covered in the event of a medical emergency can alleviate stress and anxiety.

Finding Affordable Health Insurance

One of the biggest concerns for many people when it comes to health insurance is affordability. Fortunately, there are several ways to find affordable coverage.

One option is to shop around for health insurance quotes. Shield Insurance Agency represents over 40 insurance companies and can help you find a plan that fits your needs and budget.

Contact Shield Insurance Agency at (616) 896-4600 for a free quote today.

Another option is to consider a high-deductible health plan. These plans typically have lower monthly premiums but require you to pay a higher deductible before your insurance coverage kicks in. While this can be a riskier option, it can also be a good choice for those who are generally healthy and do not anticipate needing extensive medical treatment.

Finally, you may be eligible for public health insurance programs like Medicaid or Medicare. These programs are designed to provide coverage for low-income individuals and seniors, respectively.

Choosing the Right Health Insurance Plan

When choosing a health insurance plan, it is important to consider your specific needs and budget. Some factors to consider include:

Monthly premiums: How much can you afford to pay each month for health insurance?

Deductibles: How much will you have to pay out of pocket before your insurance coverage kicks in?

Copayments and coinsurance: How much will you be responsible for paying for doctor visits, prescriptions, and other medical expenses?

Network: Does the plan include the doctors and hospitals you prefer to use?

Coverage: Does the plan cover the medical treatments and services you need?

By carefully considering these factors, you can choose a health insurance plan that provides the protection you need at a price you can afford.

In conclusion, health insurance is a crucial tool for protecting yourself and your family from the financial burden of medical expenses. Whether you choose private health insurance, public health insurance, or supplemental health insurance, it is important to find a plan that fits your needs and budget. By working with Shield Insurance Agency and carefully considering your options, you can find affordable health insurance coverage that provides the protection you need.

Contact A Shield Agent today for a review of your current policy and learn about your healthcare options:

Brianna Kornoelje, Health Benefits Advisor, Direct Line: 616.777.3012

Carlos Garcia, Health Benefits AdvisorHabla español, Direct Line: 616-777-3017

Medicare is the federal health insurance program for:

People who are 65 or older

Certain younger people with disabilities

People with End-Stage Renal Disease (permanent kidney failure requiring dialysis or a transplant, sometimes called ESRD)

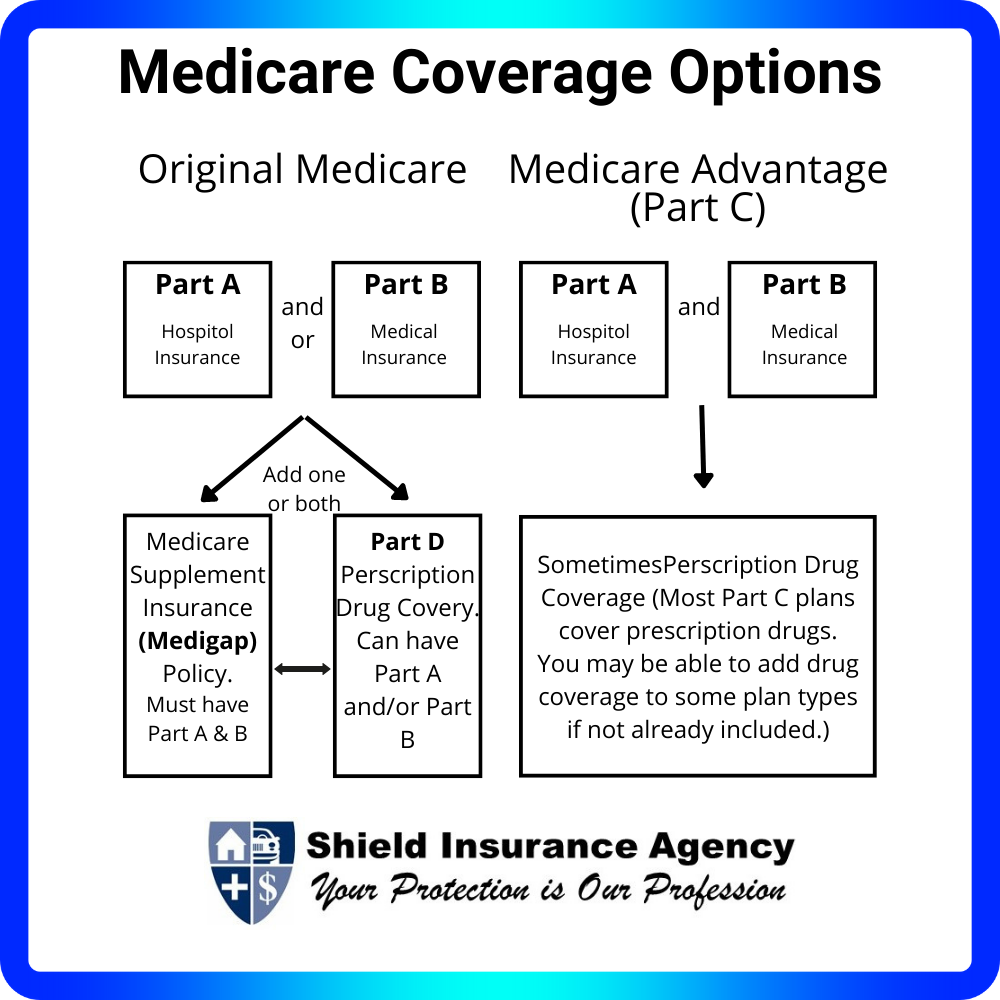

What are the parts of Medicare?

The different parts of Medicare help cover specific services:

Medicare Part A (Hospital Insurance) Part A covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care.

Medicare Part B (Medical Insurance) Part B covers certain doctors’ services, outpatient care, medical supplies, and preventive services.

Medicare Part D (prescription drug coverage) Helps cover the cost of prescription drugs (including many recommended shots or vaccines).

Part A & Part B Premiums

Most people don’t pay a monthly premium for Part A.

You usually don’t pay a monthly premium for Part A if you or your spouse paid Medicare taxes while working for a certain amount of time. This is sometimes called “premium-free Part A.”

If you don’t qualify for premium-free Part A, you can buy Part A.

If you aren’t eligible for premium-free Part A, you may be able to buy Part A. You’ll pay up to $506 each month in 2023. If you paid Medicare taxes for less than 30 quarters, the standard Part A premium is $506. If you paid Medicare taxes for 30–39 quarters, the standard Part A premium is $278.

Most people will pay the standard Part B premium amount. The standard Part B premium amount in 2023 is $164.90. If your modified adjusted gross income as reported on your IRS tax return from 2 years ago is above a certain amount, you’ll pay the standard premium amount and an Income Related Monthly Adjustment Amount (IRMAA). IRMAA is an extra charge added to your premium.

Original Medicare includes Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance). You pay for services as you get them. When you get services, you’ll pay a deductible at the start of each year, and you usually pay 20% of the cost of the Medicare-approved service, called coinsurance. If you want drug coverage, you can add a separate drug plan (Part D).

Original Medicare pays for much, but not all, of the cost for covered health care services and supplies. A Medicare Supplement Insurance (Medigap) policy can help pay some of the remaining health care costs, like copayments, coinsurance, and deductibles. Some Medigap policies also cover services that Original Medicare doesn’t cover, like emergency medical care when you travel outside the U.S.

Medicare Advantage is Medicare-approved plan from a private company that offers an alternative to Original Medicare for your health and drug coverage. These “bundled” plans include Part A, Part B, and usually Part D. Plans may offer some extra benefits that Original Medicare doesn’t cover — like vision, hearing, and dental services. Medicare Advantage Plans have yearly contracts with Medicare and must follow Medicare’s coverage rules. The plan must notify you about any changes before the start of the next enrollment year.

In October 2020, the federal government issued the “transparency in coverage” final rule under the Federal No Surprises Act. The rule provides protection against balance or “surprise” billing under certain circumstances, and phases in new transparency requirements on most group health plans and health insurers. The purpose of the requirements is to enable consumers to make informed healthcare purchasing decisions.

What is “balance billing” (sometimes called “billing surprises”)?

When you see a doctor or other health care provider, you may owe certain out-of-pocket costs, such as a copayment, coinsurance, and/or a deductible. You may have other costs or have to pay the entire bill if you see a provider or visit a healthcare facility that isn’t in your health plan’s network.

Nonparticipating describes providers and facilities that haven’t signed a contract with your health plan. Nonparticipating providers may be permitted to bill you for the difference between what your plan agreed to pay and the full amount charged for a service. This is called balance billing. This amount is likely more than in-network costs for the same service and might not count toward your annual out-of-pocket limit.

Surprise billing is an unexpected balance bill. This can happen when you can’t control who is involved in your care, such as when you have an emergency or schedule a visit at a participating facility but are unexpectedly treated by a nonparticipating provider.

Your rights and protections against Surprises

When you get emergency care or get treated by a nonparticipating provider at a participating hospital or ambulatory surgical center, you are protected from balance or surprise billing. Services you are protected from balance billing for:

Emergency services

If you have an emergency medical condition and get emergency services from a nonparticipating provider or facility, the most the provider or facility may bill you is your plan’s in-network out-of-pocket amount, such as copays, coinsurance, and deductibles. You can’t be balance billed for these emergency services. This includes services you may get after you’re in stable condition unless you give written consent and give up your protections not to be balanced billed for these post-stabilization services.

Michigan law also protects you from balance billing and requires that you pay only your in-network cost-sharing amounts for (i) covered emergency services provided by an out-of-network provider at an in-network facility or out-of-network facility; (ii) covered nonemergency services provided by an out-of-network provider at an in-network facility if you do not have the ability or opportunity to choose an in-network provider; and (iii) any healthcare services you receive at an in-network facility from an out-of-network provider within 72 hours of receiving services from that facility’s emergency room.

Certain services at a participating hospital or ambulatory surgical center

Medical Insurance is a crucial aspect of our lives that we often overlook until we need it. It provides us with financial protection against unexpected medical expenses, which can be quite expensive. Health insurance covers a wide range of medical services, including doctor visits, hospitalization, surgeries, and prescription drugs. In this blog post, we will discuss the benefits of health insurance and why it is essential to have.

One of the most significant benefits of medical health insurance is that it helps you manage your medical expenses. With health insurance, you pay a monthly premium, and in return, your insurance company covers a portion of your medical expenses. This means that you don’t have to worry about paying the full cost of medical services out of your pocket. However, it is important to note that most health insurance plans have a deductible, which is the amount you have to pay before your insurance coverage kicks in. Once you reach your deductible, your insurance company will cover a portion of your medical expenses.

Another benefit of medical insurance is that it covers prescription drugs. Prescription drugs can be quite expensive, especially if you need to take them regularly. With health insurance, you can get your prescription drugs at a lower cost, which can save you a lot of money in the long run. Some health insurance plans also cover preventive care, such as annual check-ups and screenings, which can help you detect health problems early on.

Health insurance also promotes well-being, both physical and emotional. With health insurance, you have access to medical services that can help you maintain your physical fitness and overall health. This includes regular check-ups, screenings, and access to specialists if needed. Additionally, some health insurance plans offer wellness programs that focus on nutrition and wellness, which can help you maintain a healthy lifestyle.

Emotional Health is part of Medical Insurance

Emotional health is also an important aspect of well-being, and health insurance can help you manage your mental health. Mental health services, such as therapy and counseling, can be quite expensive without insurance. With health insurance, you can get the help you need without worrying about the cost. This can be especially important for those who struggle with mental health issues, such as anxiety and depression.

Health insurance also benefits families. With a family health insurance plan, you can cover your entire family under one policy. This means that you don’t have to worry about getting individual policies for each family member. Additionally, family health insurance plans often offer lower premiums than individual plans, which can save you money in the long run.

In conclusion, health insurance is essential for managing medical expenses and promoting well-being. It covers a wide range of medical services, including doctor visits, hospitalization, surgeries, and prescription drugs. Health insurance also promotes physical and emotional health, as well as nutrition and wellness. Additionally, it benefits families by providing coverage for the entire family under one policy. If you are looking for health insurance, contact Shield Insurance Agency for all of your insurance needs at (616) 896-4600.

Health insurance is a crucial aspect of our lives that we often overlook until we need it. It provides us with financial protection against unexpected medical expenses that can arise from sickness, injury, or any other medical condition. In this blog post, we will discuss the benefits of health insurance and why it is essential to have it.

Health Insurance Bills

One of the most significant benefits of health insurance is that it helps you manage your medical bills. Medical bills can be expensive, and without insurance, you may find yourself struggling to pay them. Health insurance covers a portion of your medical expenses, which can help you save a significant amount of money. The amount of coverage you receive depends on your policy, but it can cover anything from doctor visits to hospital stays.

Another benefit of health insurance is that it helps you manage your deductibles. A deductible is the amount of money you pay out of pocket before your insurance coverage kicks in. With health insurance, you can choose a deductible that fits your budget and needs. This means that you can choose a higher deductible to lower your monthly premiums or a lower deductible to pay less out of pocket when you need medical care.

Prescriptions are another area where health insurance can be beneficial. Prescription drugs can be expensive, and without insurance, you may find yourself struggling to afford them. Health insurance can help cover the cost of prescription drugs, which can make it easier for you to manage your medical condition.

Injury and sickness are two of the most common reasons people need medical care. Health insurance can help cover the cost of medical care for both injuries and sickness. This means that you can get the medical care you need without worrying about the cost.

Medical emergencies can happen at any time, and they can be expensive. Health insurance can help cover the cost of emergency medical care, which can be a lifesaver in a medical emergency. This means that you can get the medical care you need without worrying about the cost.

Finally, health insurance can be beneficial for your family. If you have a family, you want to make sure that they are protected in case of a medical emergency. Health insurance can help cover the cost of medical care for your family, which can give you peace of mind.

In conclusion, health insurance is essential for anyone who wants to protect themselves and their family from unexpected medical expenses. It can help you manage your medical bills, deductibles, prescriptions, and emergency medical care. It can also be beneficial for your family. If you are looking for health insurance, contact Shield Insurance Agency for all of your insurance needs at (616) 896-4600. They can help you find the right policy for your needs and budget.

Christian Bowers has Down Syndrome but likes to do normal guy stuff like go bowling and play video games.

Making friends was never hard for the young man, now 24, until he finished school and found, as many people without Down Syndrome do for that matter, it’s not as easy and straightforward to maintain a social life.

Bowers’ mother, Donna Herter, watched her son sink further and further into the dumps because he didn’t have any friends to visit him.

Eventually, Herter put up a post on Facebook asking if any local guys near Rochester, Minnesota, would be interested in coming to hang out with Christian for two hours, a service for which she was willing to offer $80,00 in compensation.

A nurse on the night shift put the post up at 4:00 AM before ending her workday and going to sleep. When she woke up, it had amassed 5,000 comments.

“I was freaking out. My hands were shaking, I was sweating. I was just looking for some local guys, I didn’t want to invite like the entire world into our house,” she told CBS News.

Her friends encouraged her to calm down and take a closer look at the comments, in which she found parents offering suggestions and others volunteering to help.

She eventually found 7 fellows from Wentzville, Minnesota, who visit Christian once a week on a rotating schedule. Herter says her son goes to sleep with a smile on his face now, and is excited about life in general, and of the future as well.

Friendships are important for people born with Down Syndrome, and associations urge parents to plan for the eventuality of their child exiting school and needing to take a more precise attitude towards socializing.

Christian occasionally attends gatherings and groups of other special needs men and women his age, but craves friendship with the rest of the population as well.

“And I’ve never asked him, but I assume because it kind of makes him feel normal, just for an hour or two. ‘Hey, somebody who doesn’t have Down syndrome wants to hang out with me,’” she said.

One of the 7 friends, James Hasting, said he felt terrible that Herter had reached the point where she was trying to pay people to visit her son. Hasting, who volunteers with special needs folks, said hanging out just for a few hours to watch a movie or play video games with Christian has changed the way he looks at the world.

Many people don’t realize that Medicare decisions can have financial implications, and Medicare costs can be incorporated into comprehensive financial planning.

“When and how can I enroll in Medicare?” “How much does Medicare cost and what does it cover?” are all common questions you may have regarding your health care plan for retirement.

In addition to working closely with your financial planner, you can assess specific Medicare drug and health care plan costs by utilizing online tools.

Every day, around 10,000 members of the Baby Boomer Generation turn age 65, which is generally the age they become eligible for Medicare. [1][2] Often, this is the first time that many Baby Boomers realize that decisions around Medicare aren’t just medical decisions; Medicare decisions also have significant financial implications. Once you come to this realization, you can turn to the financial professionals on whom you depend to help make sense of Medicare and in turn help you make financially sound Medicare decisions.

Understanding Medicare can be difficult, but the Nationwide Retirement Institute® is here to help you by sharing some of the most common Medicare questions. Working with a financial professional and utilizing various planning tools can help you incorporate Medicare costs into your financial plan.

When do I enroll in Medicare?

For everyone who turns 65 and is eligible for Medicare, there’s a seven-month “initial enrollment period,” or IEP. The IEP spans from the start of the third month before your 65th birthday through the end of the third month following the month of your 65th birthday. This IEP is available regardless of whether you continue to work past age 65.

If you choose to work past age 65 and remain eligible for group health coverage provided by your employer (or your spouse’s employer), then you may choose not to enroll in Medicare during your IEP. If this is the case, you’ll have a second chance to enroll during a “special enrollment period,” or SEP. The SEP generally lasts 8 months, beginning from the month after your employment or group health coverage ends, whichever occurs first. If you do not enroll in Medicare during your IEP or SEP, then you must wait to sign up during the General Enrollment Period between January 1st and March 31st of each year; but beware that in this circumstance, you may be subject to lifelong penalties in the form of increased premiums once you do enroll.

How do I enroll in Medicare?

That depends.

If you are already receiving Social Security when you turn 65, you will automatically be enrolled in Original Medicare, which means Medicare Parts A & B. Your eligibility will be effective the first day of the month you turn 65. You will not even need to sign up. You should simply receive a red, white, and blue Medicare card in the mail around three months before your 65th birthday.

If you choose to stay on Original Medicare, you will likely want to proactively enroll in a Medicare Part D plan as well, to get prescription drug coverage. In the alternative, you may choose to enroll in a Medicare Advantage Plan, which is known as Medicare Part C. Medicare Advantage plans to replace Original Medicare and Medicare Part D, but you must proactively enroll in Medicare Advantage plans as well. You can enroll in a Medicare Advantage Plan or a Medicare Part D plan during your IEP.

Medicare.gov/plan-compare shows specific Medicare drug plans and Medicare Advantage plan costs, and you have the opportunity to call the plans you’re interested in to get more details. For help comparing plan costs, the State Health Insurance Assistance Program (SHIP) can also assist you.

If you’re not already receiving Social Security at least 4 months before turning 65, you’ll need to sign up by:

Applying online at Social Security. (If you start your online application and receive a re-entry number, you can go back to Social Security to finish your application at a later time.);

Visit their local Social Security office; or

Call Social Security at 1-800-772-1213 (TTY: 1-800-325-0778).

Nationwide teamed up with the National Council on Aging (NCOA) to create an unbiased tool to help sort through Medicare options. It’s called the NCOA My Medicare Matters® tool brought to you by Nationwide. The tool allows you to work with financial professionals so that they can assist you in the Medicare decision-making process before the completion of the enrollment process.

How much does Medicare cost?

That also depends. The first and most important thing to understand in the context of cost is that it will not be free! There are still premiums, copays, coinsurance, and deductibles to plan for.

If you sign up for Original Medicare, Part A will be free if you have paid at least 10 years of Medicare taxes. Part B will require a monthly premium of $170.10 in 2022. [3] That amount may be more if your income is high enough to cross certain thresholds.

Medicare Part D (for prescription drugs) and Medicare Advantage plans (Part C, an alternative to Original Medicare and Medicare Part D) will also have monthly premiums. The costs of those premiums will vary plan by plan and be impacted by other factors, like your age at enrollment and geographic location.

What does Medicare cover?

Not everything! That may be the simplest yet most important fact you need to understand. Medicare will not cover all medical care.

In particular, Medicare does not cover long-term care (LTC), nor vision or dental care. Also, Medicare does not cover care received outside of the USA. This means that supplemental insurance for LTC, dental and vision, and travel insurance, will be important to look into.

That being said, Medicare does cover most medical treatments and procedures. Original Medicare Parts A and B cover most basic medical services. In general, Medicare Part A covers hospitalizations (i.e., inpatient care) and Medicare Part B covers outpatient care. In addition to inpatient care, Part A also covers home healthcare in limited circumstances, as well as hospice care. Medicare Part B covers outpatient clinical services like doctor’s visits and emergency room visits, including observation. In addition to outpatient care, Part B also covers medical supplies (think splints and casts, or crutches or a wheelchair), X-rays and other radiology services, and preventive care and screening services. One important fact about this last category is that many of the preventive care and screening services covered under Part B are free; there is no coinsurance or other cost-sharing. Screenings for many cancers (including breast, cervical and vaginal, colorectal, and lung) are free, as are screenings for depression and diabetes. Many Medicare beneficiaries do not understand that these screenings, as well as many other preventive services (like flu shots), are free; consequently, they fail to seek out those services. It’s important for you to be aware of and take advantage of these free preventive and screening services to avoid delayed diagnosis and treatment of many different health conditions. Failing to do so can ultimately impact your longevity and quality of life, not to mention increase the eventual cost of treatment when an ailment’s symptoms appear later in a more advanced stage. As the adage goes, an ounce of prevention is worth a pound of cure!

Which Medicare coverage option is right for me?

For the third time in this blog, I must say it again: it depends. Decisions around Medicare are incredibly complex and depend on both medical and financial factors that are individual to each person. Many folks end up talking to their friends or neighbors for advice, but what works best for them may not work best for you! You should do some independent research and consult with your primary care physician or other medical professionals with whom you have an existing relationship so that you can make the most informed choices about the coverage and cost of your healthcare in retirement.

Where can I find out more?

If you want or need to learn more about Medicare, you can utilize other resources from Brianna, Shield Insurance Specialist. We are here to help answer all Medicare coverage questions.

This information is general in nature and is not intended to be tax, legal, accounting, or other professional advice. The information provided is based on current laws, which are subject to change at any time, and has not been endorsed by any government agency.

Nationwide and its representatives do not give legal or tax advice. Please consult an attorney or tax advisor for answers to legal questions.

My Medicare Matters® is a registered trademark of the National Council on Aging.

Nationwide and NCOA are separate and non-affiliated companies.

Nationwide Investment Services Corporation (NISC), member FINRA, Columbus, Ohio. The Nationwide Retirement Institute is a division of NISC.